Insights from COVID-19 References in CAMs

Subscriber Content

Pandemic Patterns: Uncovering COVID-19 Impacts through CAMs Analysis

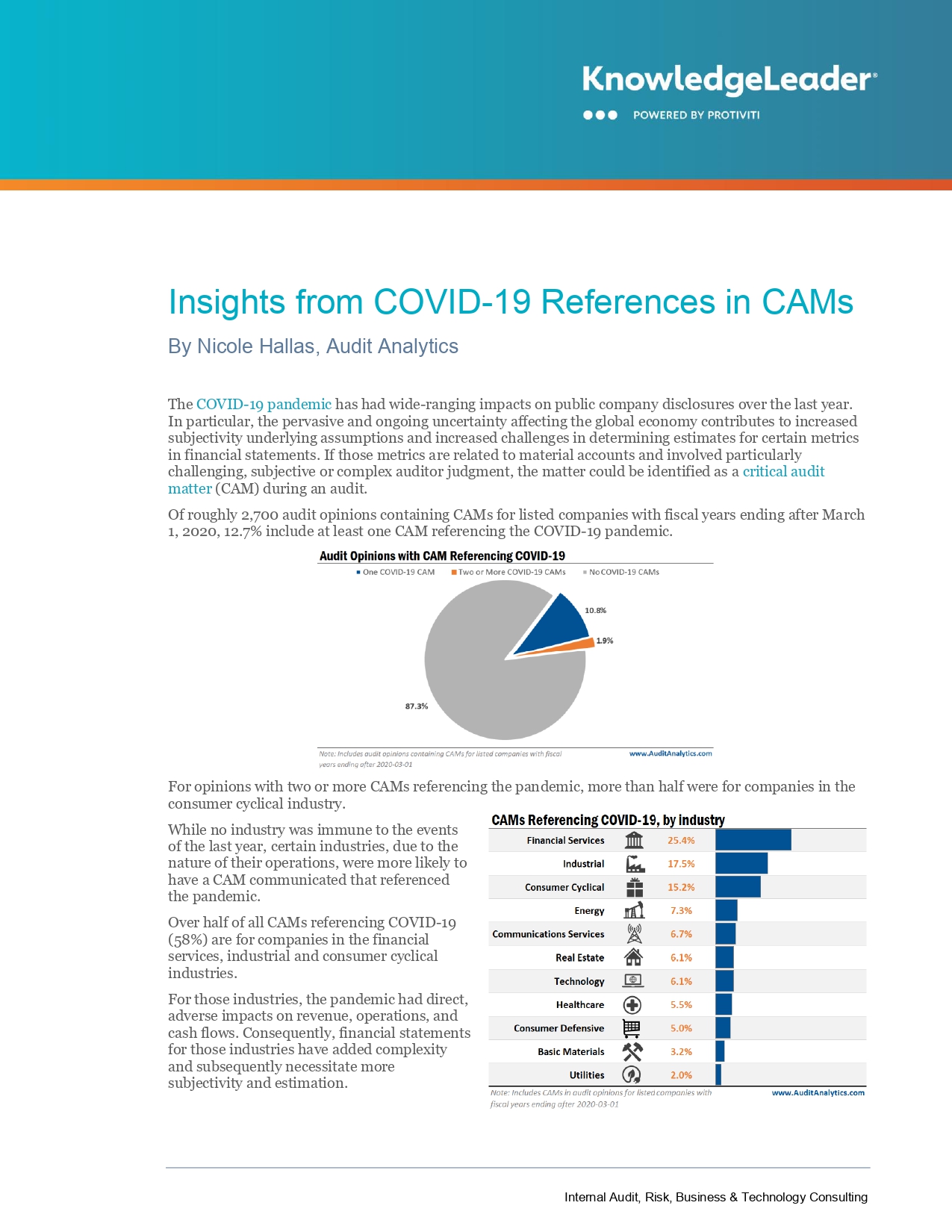

The COVID-19 pandemic has had wide-ranging impacts on public company disclosures over the last year, contributing to increased subjectivity underlying assumptions and increased challenges in determining estimates for certain metrics in financial statements. If those metrics are related to material accounts and involved particularly challenging, subjective or complex auditor judgment, it could result in the matter being identified as a critical audit matter (CAM) during an audit.

Here, Audit Analytics analyzes the pandemic’s significant impact on public company reports, including appearing in CAMs communicated in audit opinions.